Nearly Limitless Options

in One IRA

Invest in both traditional and alternative assets with a single custodian – ready to go beyond a self-directed IRA?

Investor Insights Blog|Tax-Free vs. Tax-Deferred Plans

Tax-Advantaged Accounts

Investing in retirement usually involves a bit of strategy, which a team of financial advisors can help with. One topic the advisors will probably discuss is investing in tax-free accounts vs. tax-deferred plans.

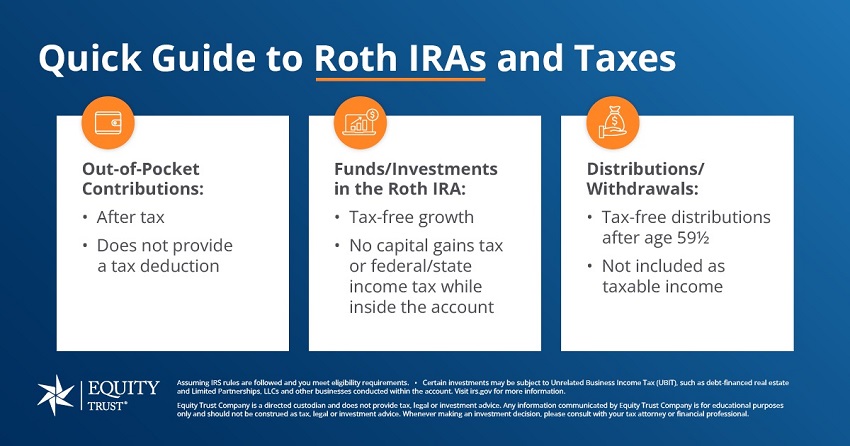

The money earned in the accounts will be tax free when withdrawn, as long as specific conditions are met. Common tax-free accounts include Roth IRAs, 529 College Savings Plans and Coverdell education savings accounts.

The money initially deposited into these accounts occurs post taxes, and these accounts are not included in income tax deductions. As the accounts earn interest, that interest will not be taxed when withdrawn according to the stipulations of the account.

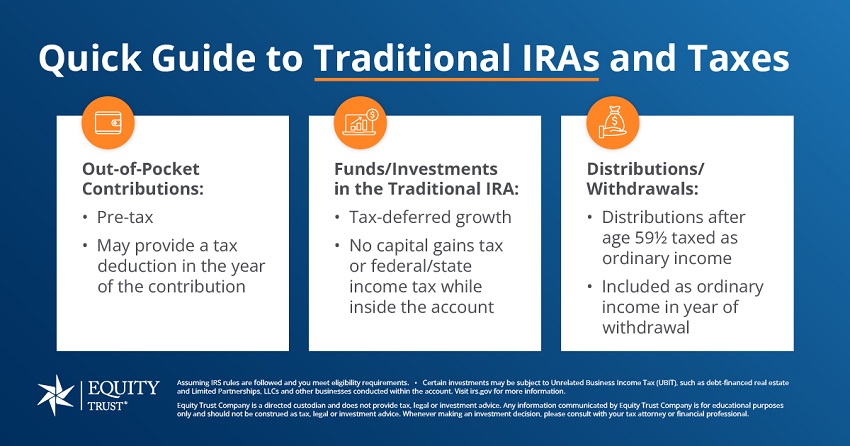

These accounts will require the investor to pay taxes on the money withdrawn from the accounts, but not on the money earned through the investment each year.

Common types of tax-deferred accounts include Traditional IRAs and 401(k)s – typically offered as employer-sponsored retirement plans. Sometimes these accounts allow investors to contribute money through the employer prior to it being taxed as well.

Because the money in these accounts can accumulate without taxation, investors often have a goal to grow the money in the account faster.

Investors also may want to investigate with their team of advisors the option of converting a tax-deferred account into a tax-free account.

When transferred, there will be taxation on the money coming from the tax-deferred account; however, it will be at the current tax prices and the current amount being transferred.

The thought is that once in the tax-free account, the money will continue to grow (as it did in the tax-deferred account), but when withdrawn at a later date, taxes will not have to be paid on a larger amount at a potentially higher tax rate.

Learn more: Investor converts assets from Traditional IRA to Roth IRA

What types of accounts does Equity Trust hold?

What are the advantages of opening a self-directed IRA?

When I roll over funds from an employer-sponsored or qualified retirement plan, do they need to go directly into a traditional IRA?

1 Equity WayWestlake, OH 44145

Terms of UsePrivacy PolicySite Map

© 2025 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 03/31/2025. 1ici.org, total assets in IRAs as of 12/2024

Terms of UsePrivacy PolicySite Map

© 2025 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 03/31/2025. 1ici.org, total assets in IRAs as of 12/2024

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.

Continue

Browse platforms and providers in private equity, cryptocurrency, lending, real estate, and precious metals asset classes – all in one place.