Nearly Limitless Options

in One IRA

Invest in both traditional and alternative assets with a single custodian – ready to go beyond a self-directed IRA?

Investor Insights Blog|Are Your IRA Contributions Tax-Deductible?

Tax-Advantaged Accounts

Are you looking for a tax deduction for this past year or to potentially lower your taxes in the future? If so, certain retirement account contributions may qualify for a tax deduction if you meet IRS eligibility requirements.

The ability to deduct your IRA contributions depends on several factors, including the type of IRA, your income, and whether you or your spouse are covered by an employer-sponsored retirement plan. For Traditional IRAs, deductions are generally available, but the amount you can deduct may be limited based on IRS rules and your Modified Adjusted Gross Income (MAGI).

If you or your spouse is covered by a retirement plan, the deduction might be reduced or phased out entirely, depending on your income and filing status. This means that if you’re married and filing jointly, your spouse’s employer-sponsored plan could also affect your deduction.

In the following sections, we’ll break down the IRS rules for this year and explain how different types of IRAs impact your eligibility for tax deductions. Remember, the deadline to contribute for 2025 is April 15, 2026.

Review the latest contribution and deduction limits here or visit the IRS website.

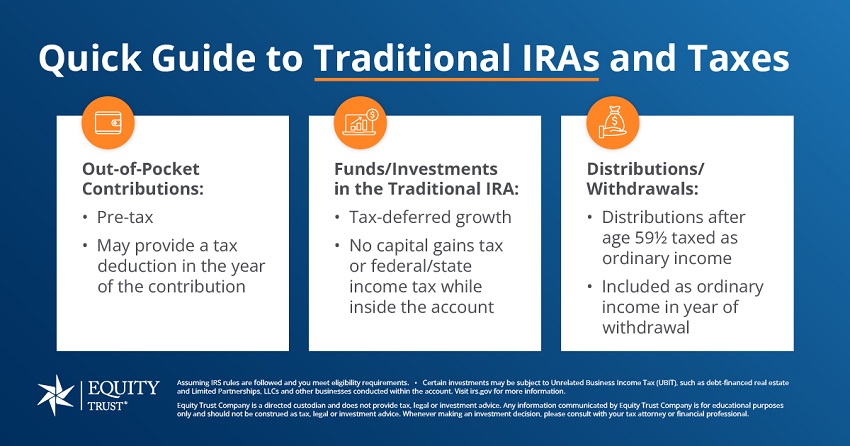

A Traditional IRA allows for tax-deductible contributions, depending on your income and whether you or your spouse are covered by an employer-sponsored retirement plan. If neither of you is covered, your contributions are fully deductible. However, if you are covered, the IRS applies income thresholds to determine your deduction amount.

The key advantage of a Traditional IRA is tax-deferred growth—your investments grow without being taxed until withdrawal, at which point they are taxed as ordinary income. While you can start taking distributions at age 59½, you must begin Required Minimum Distributions (RMDs) by age 72. Withdrawals before 59½ may incur a 10% penalty, in addition to taxes.

Video: John Bowens explains why tax deductions aren’t the only tax benefits to consider when thinking about retirement accounts.

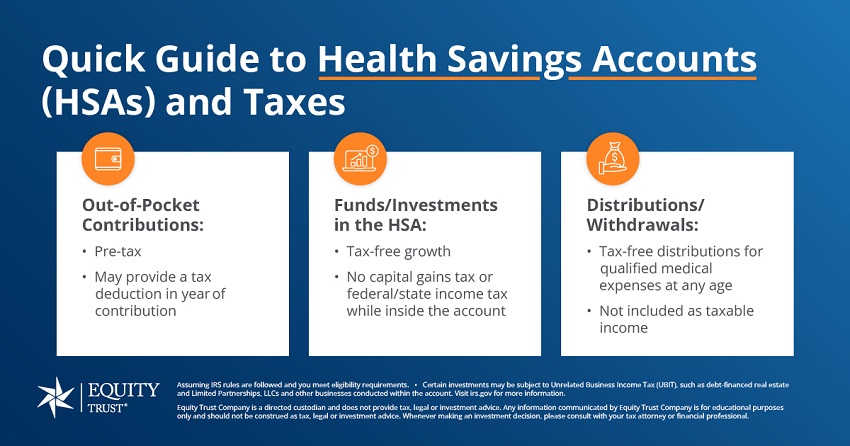

Though primarily a healthcare savings tool, an HSA offers significant tax advantages. Contributions are tax-deductible, and funds grow tax-free. Withdrawals are also tax-free if used for qualified medical expenses. HSAs provide a triple tax benefit – deductible contributions, tax-free growth, and tax-free withdrawals.

To contribute, you must be enrolled in a high-deductible health plan (HDHP). The 2025 contribution limits are $4,300 for individuals and $8,550 for families, with a catch-up contribution of $1,000 for those 55 and older. Unlike other accounts, unused HSA funds roll over year to year, making it a valuable long-term savings option for both medical and non-medical expenses after age 65.

If you own a business, you may be eligible for retirement plans with potentially larger contribution and deduction limits, in addition to an IRA and/or HSA.

Schedule a consultation with an Equity Trust IRA Counselor to discuss account options for your business.

As with all our accounts, our small business plans have the freedom to invest beyond the stock market, including alternative assets such as real estate, notes/private debt, private equity, and more.

Simplified Employee Pension (SEP) IRA

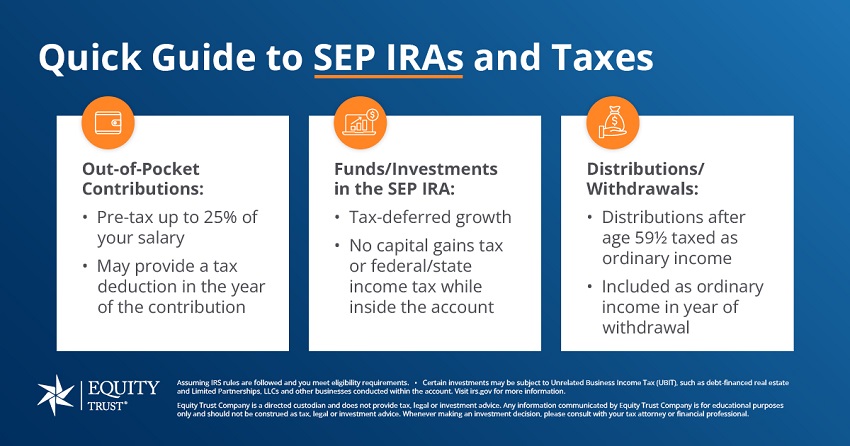

A SEP IRA is a retirement savings option designed for small business owners with up to 25 employees and self-employed individuals. Employers make contributions to SEP IRAs on behalf of their employees, and these contributions are tax-deductible for the business, making it an efficient way to lower taxable income while saving for retirement.

One of the biggest benefits of a SEP IRA is its flexibility—employers can adjust contributions from year to year based on the company’s financial performance. This account type also offers the benefit of tax-deferred growth, meaning the investments grow without being taxed until the employee withdraws the funds during retirement.

According to the IRS, the most you can deduct on your business’s tax return for SEP IRA contributions is the lesser of 25 percent of employee compensation or the annual contribution limit.

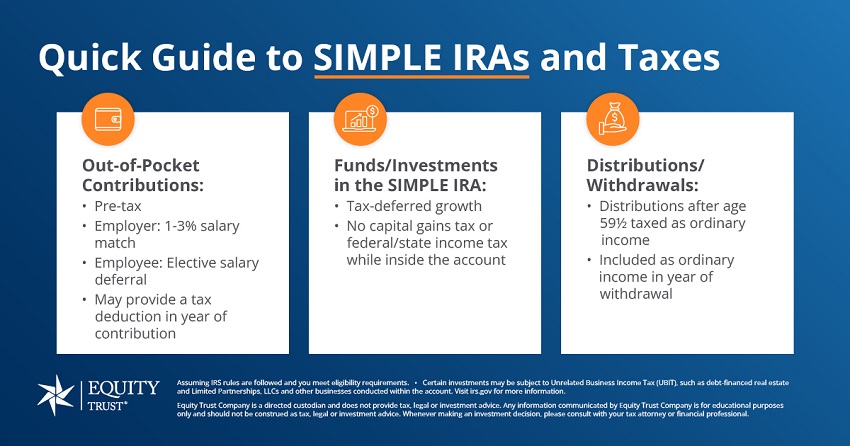

Savings Incentive Match Plan for Employees (SIMPLE) IRA

The SIMPLE IRA is designed for small businesses with generally 100 or fewer employees, offering a straightforward retirement plan that benefits both employers and employees. Employers are required to make contributions to employee accounts, which are tax-deductible, making it a valuable way to reduce business tax liabilities while providing a retirement benefit.

Employees can also contribute to their SIMPLE IRAs, and these contributions are made pre-tax, reducing their taxable income for the year. The account grows tax-deferred, meaning the funds can accumulate over time without being taxed until they are withdrawn in retirement.

Employers contribute a percent-based salary match (1-3 percent) and employees may elect to contribute through salary deferral. As the employer, you may deduct contributions made to employees’ SIMPLE IRAs on your business tax return. However, employee participants cannot deduct contributions to their SIMPLE IRA.

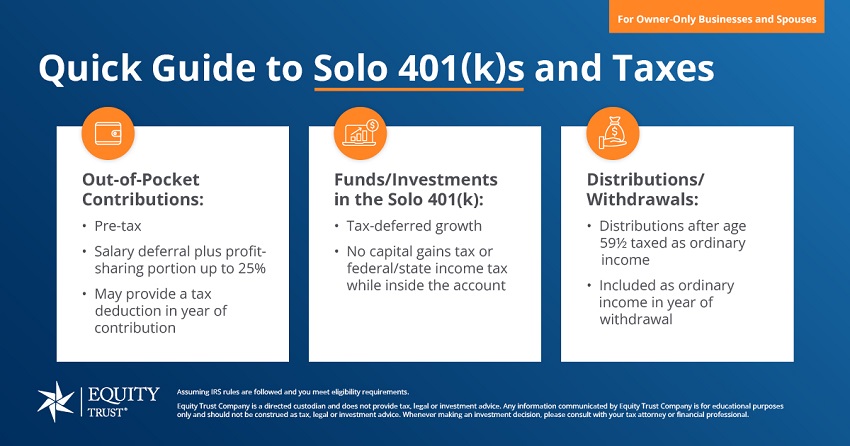

A Solo 401(k) is a retirement plan designed for self-employed individuals or small business owners with no full-time employees, offering significant flexibility and tax advantages. With a Solo 401(k), you can contribute as both the employer and the employee, allowing you to maximize your retirement savings while reducing your taxable income.

Contributions to a Solo 401(k) are made pre-tax, which means they lower your taxable income for the year and the investments grow tax-deferred until you withdraw the funds in retirement. This account is ideal for those who want to take advantage of high contribution limits and want control over their investment options. Like other retirement accounts, early withdrawals may result in penalties, and you’ll need to begin taking required distributions once you reach a certain age.

Contributions to a Roth IRA or Roth Solo 401(k) are not tax-deductible because they are made with after-tax dollars. However, the key benefit of Roth accounts is that the earnings grow tax-free, and withdrawals in retirement are also tax-free, provided certain conditions are met. Although you won’t receive a tax deduction upfront, Roth accounts can provide substantial tax savings in the long term, especially if you expect to be in a higher tax bracket during retirement.

With a self-directed IRA custodian such as Equity Trust, individuals and business owners have the opportunity to invest in alternatives outside of traditional assets like stocks, bonds, and mutual funds.

Whether you have experience in real estate, private equity, precious metals, or cryptocurrency, it’s possible to build wealth for retirement by investing in what you know best with your tax-advantaged account(s).

What are your plans for reducing your tax burden now and in the future?

Schedule a consultation with an Equity Trust IRA Counselor to discuss your tax-advantaged account options for you or your business.

Can I roll over a 401(k) account into a self-directed IRA?

Am I eligible to make a contribution? How much can I contribute?

[1] https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-seps#contributions

[2] https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-simple-ira-plans#contributions

[3] https://www.irs.gov/retirement-plans/one-participant-401k-plans

1 Equity WayWestlake, OH 44145

Terms of UsePrivacy PolicySite Map

© 2025 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 02/28/2025. 1ici.org, total assets in IRAs as of 12/2023

Terms of UsePrivacy PolicySite Map

© 2025 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 02/28/2025. 1ici.org, total assets in IRAs as of 12/2023

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.

Continue

Browse platforms and providers in private equity, cryptocurrency, lending, real estate, and precious metals asset classes – all in one place.