Nearly Limitless Options

in One IRA

Invest in both traditional and alternative assets with a single custodian – ready to go beyond a self-directed IRA?

Investor Insights Blog|Understanding Retirement Options for Your Small Business: SEP IRA vs. SIMPLE IRA

Self-Directed IRA Concepts

As your small business grows, it’s time to start thinking about the kinds of financial benefits you’d like to offer your employees. While you want to offer your employees the safety and security of a retirement plan, it can be difficult to understand what you can afford and what options require the least amount of work, maintenance, and expense.

We broke down the two main plans, SEP and SIMPLE IRAs, to explain the advantages, who qualifies, and provide examples. Some of the main differences to consider when choosing a plan are how many people your company employs, contribution limits and whether employees contribute (SEP IRA plans only allow the employer to make contributions to the account whereas a SIMPLE IRA allows more employee control).

[Related post: Differences between a Roth and Traditional IRA]

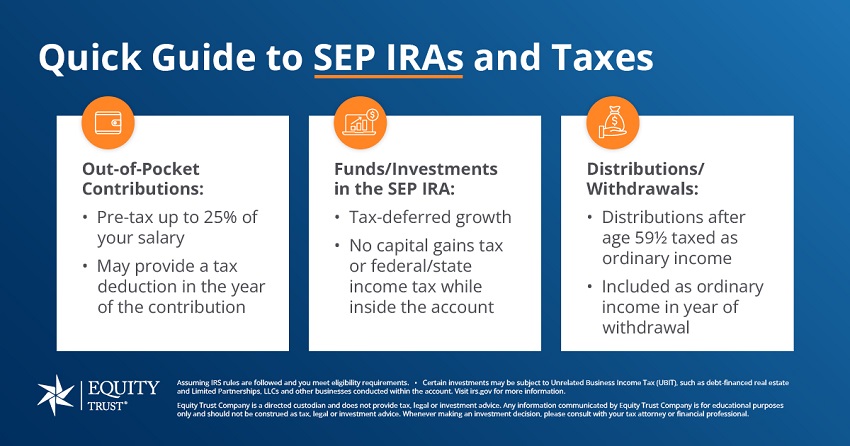

Summary: A Simplified Employee Pension (SEP or SEP IRA) is designed for self-employed individuals or small businesses with fewer than 25 employees. If you earn a self-employment income, you are allowed to save more for retirement using a SEP plan than a traditional IRA or Roth allows.

Self-employed people or small businesses with fewer than 25 employees. The SEP allows for pre-tax contributions toward retirement without getting involved in a more complex qualified plan such as a 401(k). Contributions to a SEP are tax-deductible and compound tax-deferred until withdrawn, pending that the distribution is taken after the account holder reaches 59 1/2 years of age. Additional information related to SEP accounts can be found on the IRS website.

The IRS tells us who can participate in a SEP. The employee:

An employer can use less-restrictive participation requirements than those listed, but not more restrictive ones.

The IRS states that employers’ contributions cannot exceed the lesser of:

Compare 2024 contribution limits for various IRA options.

Here are examples from the IRS to help demonstrate when a SEP is a good choice:

Example 1: Employer X maintains a calendar year SEP. The eligibility requirements under the SEP are: An employee must perform service in at least three of the immediately preceding five years, reach age 21 and earn the minimum amount of compensation during the current year.

Bob worked for Employer X during his summer breaks from school in 2016, 2017 and 2018, but never more than 34 days in any year. In July 2019, Bob turned 21. In August 2019, Bob began working for Employer X on a full-time basis, earning $30,000 in 2019. Bob is an eligible employee in 2019 because he has met the minimum age requirement, has worked for Employer X in three of the five preceding years and has met the minimum compensation requirement for 2019.

Example 2: Employer Y writes its SEP plan to provide for immediate participation regardless of age, service or compensation. John is age 18 and began working part-time for Employer Y in 2019. John is an eligible employee for 2019.

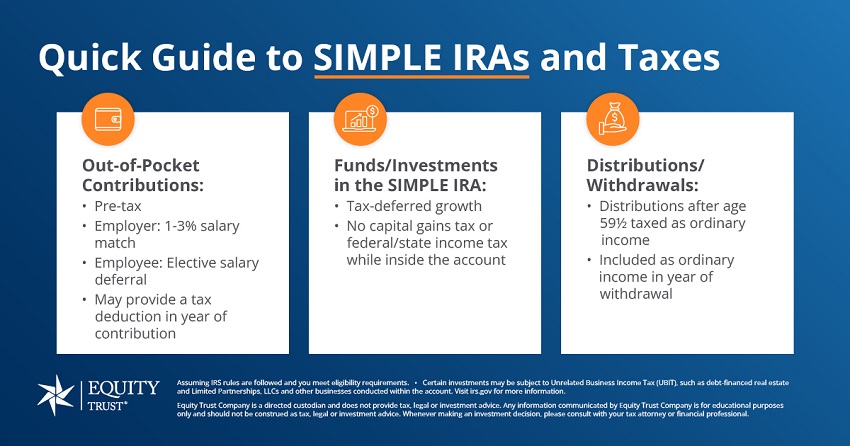

Summary: Savings Incentive Match Plan for Employees allows employees and employers to contribute to traditional IRAs set up for employees.

It is ideally suited as a start-up retirement savings plan for small employers (100 or fewer employees) not currently sponsoring a retirement plan. With a SIMPLE plan, contributions are tax-deductible, and earnings within the account are tax-free until withdrawn. Employees are also 100-percent vested, which means they are able to take all funds, including employer contributions, with them if they leave.

You can establish a SIMPLE IRA plan if you meet BOTH of the following requirements:

You can establish a SIMPLE IRA plan only if you had 100 or fewer employees who received $5,000 or more in compensation from you for the preceding year.

Under this rule, you must take into account all employees who were employed at any time during the calendar year, regardless of whether they’re eligible to participate.

The SIMPLE IRA plan generally must be the only retirement plan to which you make contributions, or to which benefits accrue, for service in any year beginning with the year in which the SIMPLE IRA plan becomes effective.

A SIMPLE IRA allows:

Employers are generally required to match each employee’s salary reduction contributions, on a dollar-for-dollar basis, up to 3 percent of the employee’s compensation. You can deduct SIMPLE IRA contributions for the tax year within which the contributions were made.

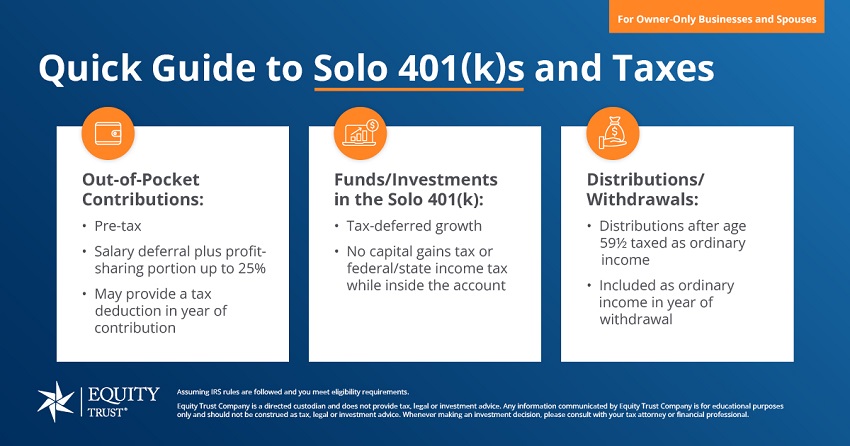

If you are the sole proprietor of your business, you and your spouse may qualify for the Solo 401(k) option, which combines elements of the SEP and SIMPLE plans.

This option offers higher contribution amounts and possible tax deductions. However, there are precise qualifications that must be met in order to be eligible. Learn more about the Solo 401(k) and see if you qualify.

For more information about the difference between these plans, Equity Trust National Education Specialist John Bowens simplifies what you need to know in this whiteboard session:

What types of accounts does Equity Trust hold?

What is a self-directed IRA?

1 Equity WayWestlake, OH 44145

Terms of UsePrivacy PolicySite Map

© 2025 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 03/31/2025. 1ici.org, total assets in IRAs as of 12/2024

Terms of UsePrivacy PolicySite Map

© 2025 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 03/31/2025. 1ici.org, total assets in IRAs as of 12/2024

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.

Continue

Browse platforms and providers in private equity, cryptocurrency, lending, real estate, and precious metals asset classes – all in one place.