Nearly Limitless Options

in One IRA

Invest in both traditional and alternative assets with a single custodian – ready to go beyond a self-directed IRA?

Investor Insights Blog|5 Potential Benefits of an HSA

Tax-Advantaged Accounts

The rising cost of health care (and health insurance) is a concern many Americans are facing today. But it’s also a concern many will face in retirement as well.

The HealthView Services’ 2021 Retirement Healthcare Costs Data Report estimates “the average healthy 65-year-old couple retiring this year can expect to pay more than $662,000 in lifetime Medicare and supplemental insurance premiums and out-of-pocket costs.”

This estimate does not include long-term care expenses which could cost tens of thousands of dollars more per year.

Fortunately, a Health Savings Account at Equity Trust could provide a tax-advantaged solution to help combat the rising costs of health care – now and in retirement.

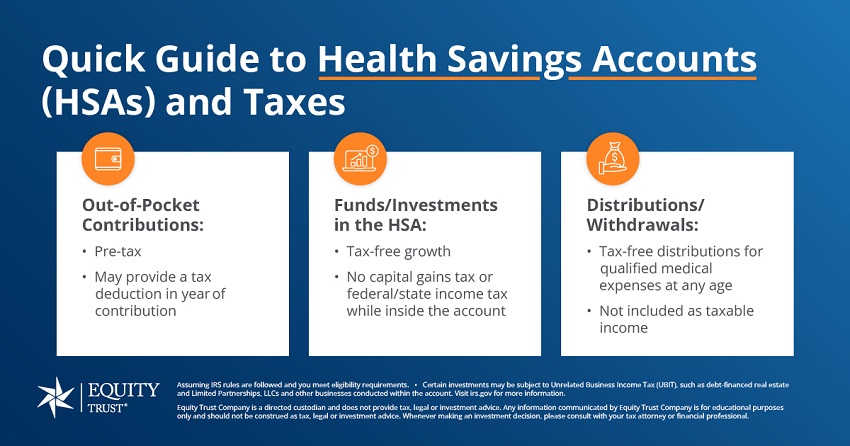

Arguably one of the most valuable features of an HSA are the tax advantages.

According to a recent CBS News Money Watch article by Ray Martin, HSAs have three tax benefits:

“No other account for long-term savings allows this triple tax-free benefit,” the article says.

Unlike self-directed IRAs and other retirement accounts, you can begin enjoying the tax-advantaged benefits of an HSA well before age 59½ without tax or penalty, as long as the funds are used for qualified medical expenses.

For example, let’s say you have $1,000 of qualified medical expenses this year, including doctor’s visits and prescription medications.

You plan to pay the expenses out-of-pocket because they are less than the $2,700 deductible you have from your High Deductible Health Plan (HDHP).

No other account for long-term savings allows this triple tax-free benefit.

Ray Martin, CBS News Money Watch

In this hypothetical example, you could contribute $1,000 to your HSA this year (potential tax deduction) and pay the expenses with a $1,000 distribution from your HSA tax-free.

Furthermore, certain insurance premiums and deductibles may be considered qualified medical expenses for an HSA.

Continuing the example, let’s assume your medical expenses exceeded your deductible and were covered by your health insurance.

You could potentially pay the $2,700 deductible with a tax-free HSA distribution, rather than out-of-pocket.

To understand the saving potential of an HSA, it may be helpful to think of it as another retirement account.

At Equity Trust, a self-directed HSA can complement your retirement accounts, providing another tax-advantaged vehicle to help you save and invest for your financial future – but with a specialized focus: health care.

In addition to helping save for health care expenses during retirement, it may also be possible to view your HSA similar to another Traditional IRA.

After you turn 65, funds distributed from an HSA for something other than qualified medical expenses are no longer subject to the 20-percent early distribution penalty and are only subject to ordinary income tax.

In essence, distributions for non-qualified medical expenses from an HSA after age 65 have the same tax treatment as funds in a Traditional IRA or 401(k). (See IRS Publication 969 for more information)

Unlike Flexible Spending Accounts (FSAs) and other medical savings accounts, HSAs are not “use-it-or-lose-it.” Account balances may be carried over from one tax year to the next.

You determine how much is contributed to your HSA each year (based on the contribution guidelines set by the IRS), and whether to pay current medical expenses from the account or save the money for future medical expenses.

It may also be possible to pay for medical expenses out-of-pocket when they are due, while saving all documentation and receipts so you can reimburse yourself with a tax-free distribution from your HSA at a later date.

There is no requirement to pay the medical expense directly with an HSA distribution – only that the distributed amount is for qualified medical expenses and is properly documented to the IRS and supported with receipts.

Let’s consider another hypothetical example where you saved all receipts, invoices, and supporting documentation for 10 years of qualified medical expenses – but never took an HSA distribution and paid them all out-of-pocket.

As long as the qualified medical expenses occurred after your HSA was established, it may be possible to reimburse yourself with a tax-free lump-sum distribution for the total amount, 10 years later.

Please consult with a tax attorney or financial professional and reference IRS Publication 969 and IRS Publication 502 before making any financial or investment decisions.

Finally, similar to an IRA, your HSA is entirely portable and stays with you even if you change jobs. However, if your new employer doesn’t offer a high-deductible health plan (or you decide to change plans and are no longer enrolled in a HDHP), you can no longer contribute to your HSA but can still invest your current funds.

Finally, a self-directed HSA at Equity Trust is more than a savings account.

Like all accounts at Equity Trust, you can invest your HSA in what you know best – whether it’s real estate, notes, private equity and a variety of alternative assets, or possibly traditional assets like stocks, bonds and mutual funds.

With an HSA at Equity Trust, you have the opportunity to build tax-free health care savings for you and your family – now and in the future.

What types of accounts does Equity Trust hold?

1 Equity WayWestlake, OH 44145

Terms of UsePrivacy PolicySite Map

© 2025 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 03/31/2025. 1ici.org, total assets in IRAs as of 12/2024

Terms of UsePrivacy PolicySite Map

© 2025 Equity Trust®. All rights reserved.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Equity Institutional services institutional clients of Equity Trust Company. Brokerage Services Available Through ETC Brokerage Services, Member SIPC, and FINRA. *Founded in 1974 | Self-Directed IRA Custodian since 1983. The predecessor business to Equity Trust Company was established in 1974 and the IRS approved as a custodian in 1983. **Assets under custody and administration as of 03/31/2025. 1ici.org, total assets in IRAs as of 12/2024

You are leaving trustetc.com to enter the ETC Brokerage Services (Member FINRA/SIPC) website (etcbrokerage.com), the registered broker-dealer affiliate of Equity Trust Company. ETC Brokerage Services provides access to brokerage and investment products which ARE NOT FDIC insured. ETC Brokerage does not provide investment advice or recommendations as to any investment. All investments are selected and made solely by self-directed account owners.

Continue

Browse platforms and providers in private equity, cryptocurrency, lending, real estate, and precious metals asset classes – all in one place.